")

There are a lot of methods to do credit score spreads.

Merchants can fine-tune their credit score spreads to realize a selected risk-to-reward ratio primarily based on market outlook, volatility, and private threat tolerance.

They’ll shift the stability between potential revenue and most loss.

Understanding learn how to handle these variables is crucial for optimizing returns whereas sustaining acceptable threat publicity.

Let’s find out how.

They apply to each bull put credit score spreads and bear name credit score spreads, however we’ll use put credit score spreads in our instance.

Contents

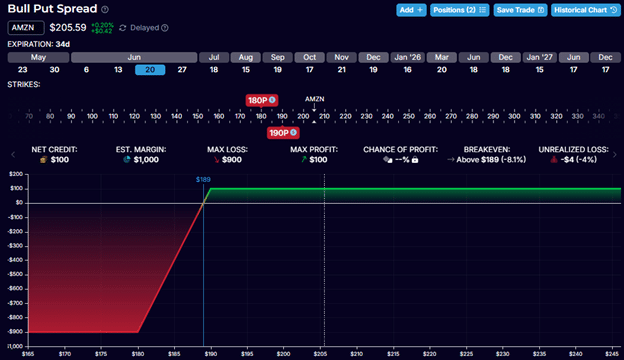

We begin with a typical out-of-the-money (OTM) bull put credit score unfold.

Take Amazon (AMZN) for instance.

Date: Could 16, 2025

Worth: AMZN @ $205.59

Purchase one Jun 20 AMZN $180 putSell one Jun 20 AMZN $190 put

Credit score: $100

The chance graph at expiration seems to be like this:

The preliminary credit score acquired of $100 is the utmost return we are able to get from this commerce.

That is the utmost reward.

The max threat, as seen by the bottom level on the chance graph, is $900.

That is the utmost lack of the commerce.

The max loss is said to the width of the unfold; the higher the width, the higher the chance.

If the commerce goes utterly dangerous with the worth of AMZN beneath $180 per share at expiration, it means we now have to purchase AMZN at $190 per share (the brief strike) and promote it at $180 per share (the lengthy strike) – a lack of $10 per share.

Since one contract represents 100 shares, the unfold threat is $1000.

Contemplating the credit score of $100 that the dealer acquired initially, the web loss within the worst-case state of affairs is $900.

The chance-to-reward on this commerce is 9-to-1.

Danger-to-reward ratio = Max Danger / Max Reward = $900 / $100 = 9

The dealer is risking $9 to make $1.

You’ll be able to certainly regulate the risk-to-reward ratio by altering the width of the unfold.

Nevertheless, for the aim of right now’s dialogue, we’ll concentrate on adjusting the risk-to-reward by shifting the situation of the unfold on the choice chain.

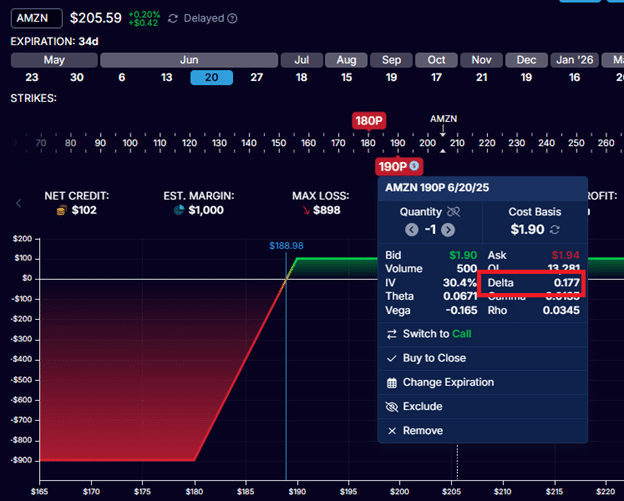

The choice chain or the analytics software program exhibits that the $190-strike put choice within the final instance is on the 17-delta.

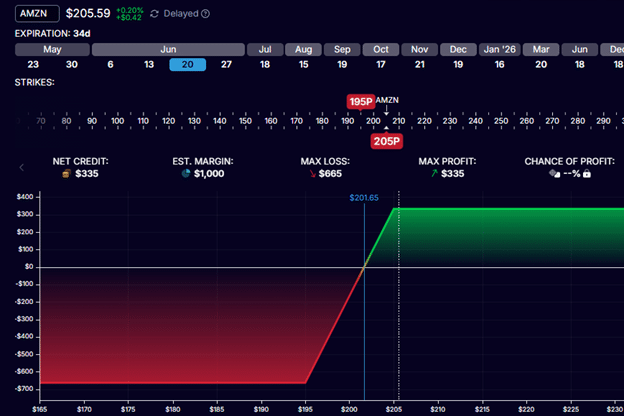

Now let’s have a look at the credit score unfold of the identical width however nearer to the cash:

Right here, we’re promoting the $205-strike put choice and shopping for the $195 put choice.

The brief strike of $205 is on the 45-delta.

The dealer collected $335 from promoting this credit score unfold.

The chance-to-reward ratio on this instance is 2-to-1.

How do I do know?

As a result of the red-shaded space of the chance graph is twice as tall because the green-shaded space, that implies that the chance is twice as a lot because the reward.

Or you are able to do the maths.

The max threat is:

$1000 – $335 = $665

And so the chance to reward is $665 / $335 = 2

You would possibly typically hear some merchants say they need to accumulate one-third the width of the strikes.

That is an instance of such.

The width of the strikes is $10.

The credit score collected per share is $3.35, which is one-third of the width.

If the reward is one-third of the width, the chance is the remaining two-thirds.

The dealer is risking two {dollars} to make one greenback.

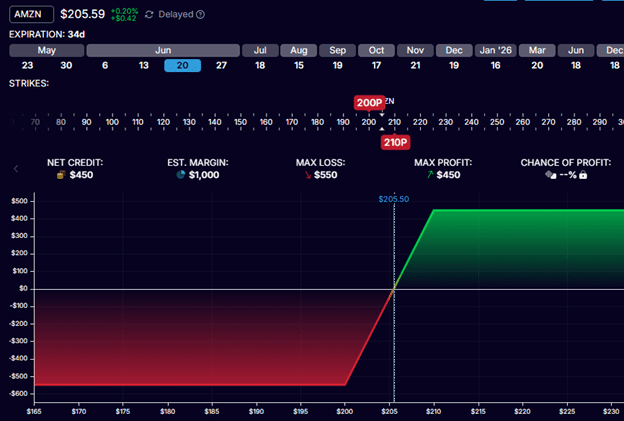

Shifting the put credit score unfold nonetheless additional to the fitting on the worth axis, we now have an at-the-money credit score unfold:

Get Your Free Put Promoting Calculator

With AMZN at $205, the dealer is promoting the $210-strike put choice and shopping for the $200-strike put.

The $210 strike is within the cash (as a result of AMZN’s value is beneath the put strike value).

And the $200 strike is out-of-the-money (as a result of AMZN’s value continues to be above the put strike value).

The credit score unfold is at-the-money (ATM) as a result of its legs are straddling the inventory value.

On this case, we now have practically a one-to-one risk-to-reward, as you possibly can see, and the inexperienced space is about equal to the crimson space.

To be exact:

Danger-to-reward ratio = $550 / $450 = 1.2

The place the max revenue of $450 and max threat of $550 have been already calculated for us by OptionStrat within the above screenshot.

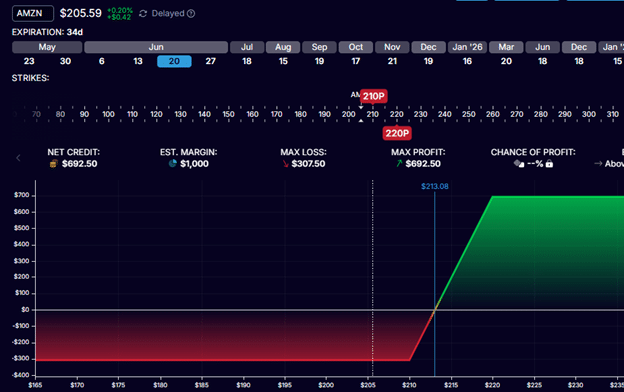

We are able to transfer each of the put credit score unfold strikes to be within the cash like this:

Promoting the $220 strike and shopping for the $210 strike.

The worth is beneath each put strikes.

So, each legs of this put credit score unfold within the cash.

Now, the chance is smaller than the reward.

Danger-to-reward = $307.50 / $692.50 = 0.44

it one other method, the reward is about twice as a lot as the chance.

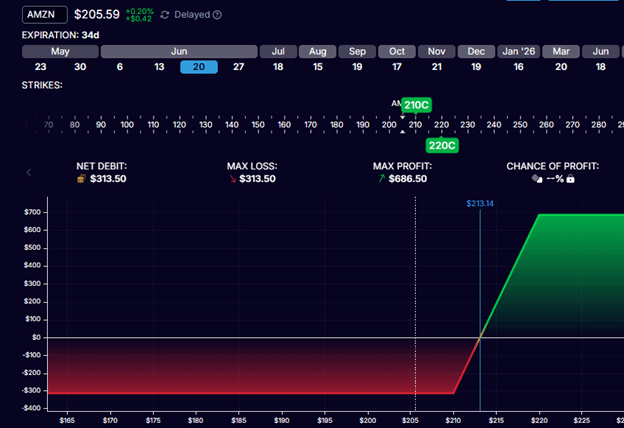

Sure, this ITM put credit score unfold is equal to the next OTM name debit unfold, the place the dealer sells the $220-strike name choice and buys the $210-strike name choice.

As a result of these are name choices and each name strikes are above the present inventory value, that is an out-of-the-money name debit unfold.

The dealer needed to pay $313.50 to enter into this unfold.

And that’s additionally the utmost potential loss.

The chance-to-reward this OTM name debit unfold is identical because the ITM put credit score unfold:

Danger-to-reward = $313.50 / $686.50 = 0.45

As a result of the bid/ask distinction is smaller in OTM choices than in ITM choices, this OTM name debit unfold tends to have a tighter bid/ask than the equal ITM put credit score unfold.

So, if a dealer is searching for the sort of risk-to-reward, it’s preferable to commerce the OTM name debit unfold as an alternative of the ITM put credit score unfold.

In addition to that, all the pieces else is identical between the 2 – together with the Greeks.

One of many traits of credit score spreads is that they’ve a optimistic theta the place the P&L can accrue with time even when the inventory value doesn’t transfer.

That is true solely of OTM credit score spreads.

Listed below are the thetas for every of our examples:

OTM $190/$180 put credit score unfold: theta = 2.47

Close to-the-money $205/$195 put credit score unfold: theta = 0.13

ATM $210/$200 put credit score unfold: theta = -1.6

ITM: $220/$210 put credit score unfold: theta = -3.8

As we transfer the unfold nearer to the cash, we get much less and fewer theta.

The ATM credit score unfold shall be near zero.

Shifting the unfold within the cash, the theta turns into unfavorable, inflicting the unfold to behave extra like a debit unfold.

Credit score spreads behave in a different way and have completely different risk-to-reward relying on the place you place them on the choice chain.

If credit score spreads don’t really feel comfy to you, maybe it isn’t on the risk-reward ratio acceptable to your threat tolerance and/or commerce thesis.

A really far out-of-the-money credit score unfold could trigger one dealer to really feel like he/she is getting little or no reward for the potential threat – like selecting up pennies in entrance of a steam curler.

If that’s the case, strive a credit score unfold nearer to the cash.

You get an even bigger reward and decrease threat.

One other dealer would possibly discover that the brief strike of the unfold is uncomfortably near the inventory value.

If that’s the case, transfer the unfold additional out.

Like attempting on footwear, you need to strive credit score spreads at completely different strikes and risk-to-reward to search out ones that fit your needs.

We hope you loved this text on adjusting the risk-to-reward ratio of credit score spreads.

If in case you have any questions, ship an e-mail or depart a remark beneath.

Commerce protected!

Disclaimer: The data above is for academic functions solely and shouldn’t be handled as funding recommendation. The technique introduced wouldn’t be appropriate for buyers who are usually not conversant in trade traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.